Staff Writer

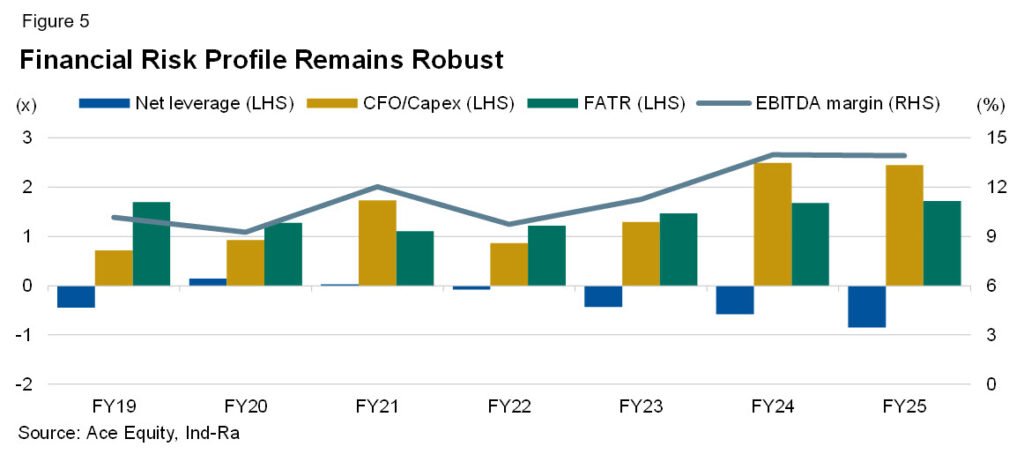

New Delhi: India Ratings and Research (Ind-Ra) believes the Indian passenger vehicle (PV) sector is entering a structurally positive but execution-sensitive capex cycle, with cumulative investments of INR3.2 trillion–3.5 trillion over FY26–FY30, underpinning electric vehicle (EV) transition, export scale-up, and premiumisation. While long-term earnings and return metrics could structurally improve, investors should expect near-term moderation in return on capital employed (ROCE), potential capacity utilisation gaps, and execution risks around EV adoption. With EV capex accounting for 60%–70% of investments and exports already contributing nearly 18.7% to volumes in FY26, the sector’s growth drivers remain strong; however, EV penetration of only 3%–4% and infrastructure bottlenecks indicate a phased payoff. Strong balance sheets (net leverage: negative 0.8x; cash flow from operations (CFO)/capex nearly 2.4x) mitigate downside risks, keeping credit profiles resilient, despite elevated capex.

“The Indian PV sector is currently in the midst of a structurally driven capex cycle, led by EV transition and export scale-up, with investments increasingly front-loaded relative to demand. Near-term return metrics, especially for the EV segment, are likely to remain under pressure given the gradual pace of EV adoption. Nevertheless, strong balance sheets of incumbent original equipment manufacturers (OEMs) and robust internal accruals from their existing operations provide sufficient financial flexibility to absorb this investment phase without materially weakening credit profiles, the risk profile remains higher for pure-play EV entrants and new global players entering India, where elevated capital intensity and dependence on demand ramp-up could delay return normalisation,” says Shruti Saboo, Director, Corporate Ratings, Ind-Ra.

EV Capex Will Dominate, but Returns Will Lag Before Scaling Up: Ind-Ra opines that EV-led investments will structurally strengthen the PV sector’s competitive positioning, but returns will remain under pressure in the near term, due to front-loaded capital deployment and a gradual demand ramp-up.

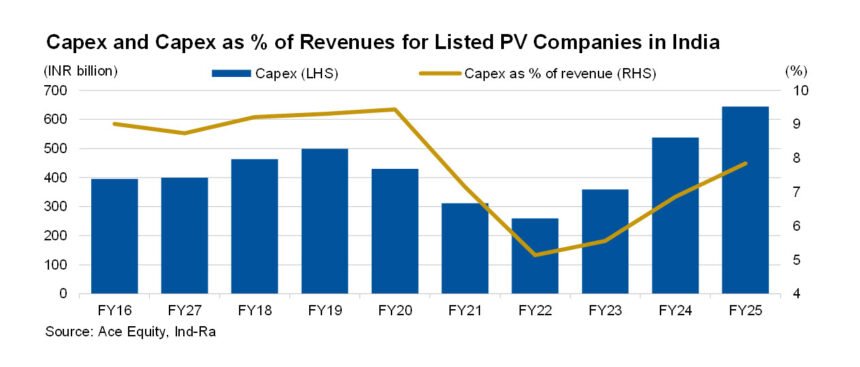

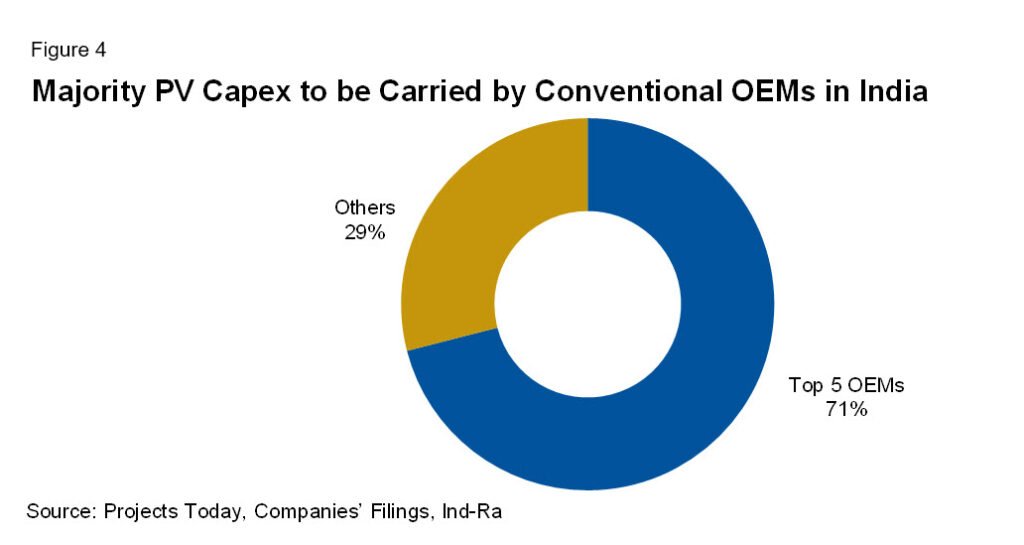

The sector is witnessing a decisive shift toward EV-led investments, with 60%–70% of the announced capex directed toward EV platforms, battery technology, and ecosystem development. The top five OEMs account for over INR2,000 billion of the planned investments, with execution likely to be phased and contingent on demand. Historically, although capex intensity averaged 9%–10% of revenues during FY15–FY20, it moderated to 6%–8% in recent years, due to improved utilisation and efficiencies. However, absolute capex increased to INR644 billion in FY25 (FY22: INR259 billion), highlighting scale expansion despite disciplined intensity.

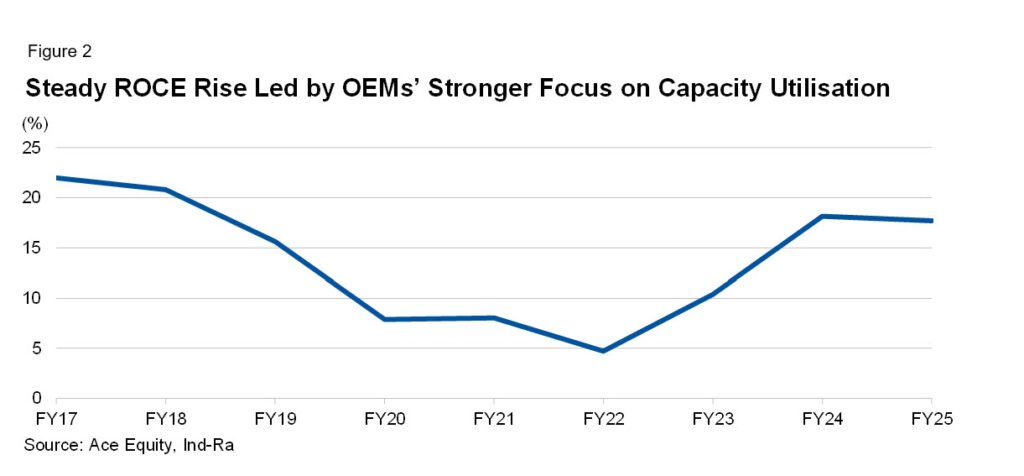

While ROCE remained healthy at 15%–20% over FY23–FY25, it is likely to moderate in the near term, due to rising capital employed ahead of earnings generation. Over the medium term, Ind-Ra expects the ROCE to improve with EV scale-up, platform standardisation, and operating leverage gains.

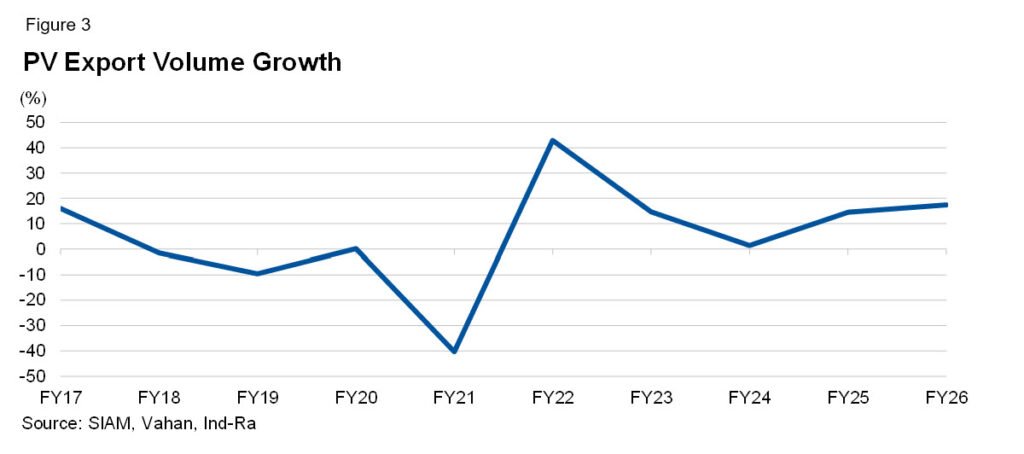

Ind-Ra expects export growth to be a key structural lever, supporting capacity absorption, improving asset utilisation, and enhancing the long-term return profile of current investments. Exports scaled up to 18.7% of PV volumes in FY26, expanding at a CAGR of about 12% over FY23–FY26. This indicated India’s increasing role as a global manufacturing hub for small cars and small utility vehicles across emerging markets.

OEMs are aligning capex towards flexible, globally compliant production lines that can cater to both domestic and export demand, reducing earnings volatility and enhancing utilisation across cycles. India’s cost competitiveness and strong auto component ecosystem further support export growth, providing supply chain resilience and a partial hedge against geopolitical and demand-side risks.

Ind-Ra expects capacity expansion to outpace demand in the near term, resulting in temporary utilisation pressure before normalising with demand recovery and EV adoption. The industry is adding 3 million–3.5 million units of capacity over an existing base of 6.1 million units, indicating a significant scale-up aligned with medium-term demand expectations.

Leading OEMs’ capacity utilisation levels stood at 60%–85% in 2025 and are likely to moderate as new capacities are commissioned. Notably, continued investments by OEMs with sub-50% utilisation indicate that capex is strategically driven by EV transition and technology preparedness rather than near-term demand visibility. This creates a temporary mismatch between supply addition and demand absorption. Over the medium term, growth in SUVs, exports, and EV penetration are expected to support utilisation recovery.

Ind-Ra believes strong balance sheets and internal accruals will enable OEMs to absorb elevated capex without materially weakening credit profiles. As of FY25, the sector demonstrated strong financial flexibility with the net leverage remaining at negative 0.8x and CFO/capex at about 2.4x, indicating robust internal funding capacity.

The agency expects planned investments to be funded through a mix of internal accruals, parent support, and equity infusion through EV-focused subsidiaries, limiting reliance on external debt. Government support through schemes such as Production-linked Incentive (PLI) might enhance project viability and improve returns over time. However, any shift towards materially debt-funded capex or delays in EV monetisation could lead to a moderation in the credit metrics and will remain a key rating monitorable.

Regulatory Support and PLI Incentives Provide Structural Tailwinds: Government support remains a key enabler of the EV capex cycle, with INR259 billion PLI-Auto scheme. While 82 companies have been approved under PLI-Auto, with around INR357 billion in committed investments as of December 2025, execution has remained gradual, with only INR23.8 billion in incentives disbursed as of February 2026. PLI incentives (8%–18% of incremental sales) aid in improving project viability, accelerating localisation (50% domestic value addition requirement), and driving investments across OEMs and auto component companies. However, gaps persist in battery cell manufacturing. Sustained policy support and timely disbursements remain critical for a gradual ramp-up in EV-related capex.

EV Adoption Risk Remains Key Swing Factor for Returns: Ind-Ra views EV adoption as the single-most critical variable determining the success of capex cycle, with infrastructure gaps posing a meaningful downside risk to returns. Despite strong OEM commitment, EV penetration remains low at 3%–4% of PV volumes, constrained by limited charging infrastructure, particularly outside urban centres. A lag in charging ecosystem development could result in underutilisation of EV-dedicated capacities, delaying return generation.

While technological advancements in battery efficiency may support adoption, infrastructure readiness remains the key bottleneck. Sustained coordination among OEMs, policymakers and private players will be essential to bridge this gap and unlock the full potential of EV investments. Additionally, a supplier ecosystem will be critical for EV adoption. Indian auto component players are gradually transitioning from internal combustion engine-linked products to EV-focused areas, with investments coming in battery management systems, motors, controllers and lightweight materials. Despite strong PV OEM capex, the component sector is largely maintaining steady-state investments as OEM capex tends to be front-loaded, whereas supplier investments are more staggered, typically scaling up with clearer volume visibility and platform commitments. As of now, the domestic EV supply chain remains underdeveloped—particularly in battery cells, which account for 35–40% of EV costs and are still largely imported.

Ratings and Credit Trends: Stable Outlook with Selective Monitoring of EV Execution Risks: Ind-Ra maintains a stable rating outlook on most PV OEMs for FY27, supported by strong credit profiles, while closely monitoring execution risks arising from the ongoing capex cycle. Ratings across leading OEMs continue to reflect strong liquidity, conservative leverage, and disciplined financial policies, despite elevated investment commitments.

Recent geopolitical developments, including tensions in the Middle East, could act as a structural catalyst for EV adoption in India, potentially bringing forward demand realisation and supporting faster absorption of EV-led capex. However, the durability of this demand uptick will depend on affordability dynamics and an improvement in the charging infrastructure. Key rating considerations include stability in operating cash flows, ability to maintain liquidity buffers, and disciplined funding strategies. At the same time, Ind-Ra is monitoring EV-related execution risks, including slower adoption, utilisation pressure, and capital allocation through subsidiaries.